An investigative report about the Goodwill Industries affiliate in Omaha in a local paper started by looking at high compensation levels for the Omaha executives, but then continued to look at the payment of hourly rates for disabled workers less than the minimum wage. Then the issues of conflict of interest between board and staff, nepotism, and even the repackaging of foreign-made goods sold under “Made in America” labels were revealed. As community support waned, there was serious discussion of withdrawing the county-granted organizational exemption from property tax.

These revelations have dramatically changed the way Goodwill Omaha functions, and the charity will be heavily scrutinized for years to come. The property tax exemption was just extended, but time will be needed to rebuild community trust.

Now the search is on for a new executive, and the charity should be carefully following the IRS prescribed procedures. These are detailed in ERI’s recent Guide to Setting Nonprofit Executive Compensation.

To summarize here, the IRS wants a charity to pay “reasonable compensation” – that is, “an amount as would ordinarily be paid for like services by like enterprises under like circumstances.” So what does that really mean? The IRS definitions follow:

- Like services: Jobs with substantially similar duties and responsibilities (e.g., the number of employees managed, the size of the budget or assets managed, hours worked, and geographic scope).

- Like enterprises: Organizations similar in size (based on such factors as annual budget, assets, number of employees, or number of persons served). Equally important, organizations similar in services provided or purpose (e.g., universities compared with universities, day care centers with day care centers, etc.) If the charity can show that tax-exempt and for-profit entities compete for the same pool of specialized talent, then the for-profit data can be used for some, but not all, of the comparative data.

- Like circumstances: All forms of compensation included in the comparison (consider expense or housing allowances, plus other financial benefits). A review of geographic differences might call for adjustments. Also if sufficient comparable data are not available for the geographic area, then comparables from a larger geographic region might be necessary, in addition to potential cost-of-living adjustments.

The IRS has decided that compensation will be presumed reasonable, unless proven otherwise, if the organization follows a set of standard procedures, creating what is termed a “rebuttable presumption of reasonableness.” This presumption puts the burden of proving that compensation is not reasonable on the IRS, not the organization. The IRS requires these criteria for establishing the rebuttable presumption:

- Approval by the authorized body of the organization (usually the full Board of Directors), but with no participation by anyone who might be affected by the decision on compensation.

- Use of “appropriate data” to determine comparability prior to making a decision. That means looking at what nonprofit employers with similar missions, and similar budget sizes, located in the same area, or a similar geographic region, pay their executives.

- Documentation of the basis for the salary decision (who was involved with reviewing comparable data and his/her “independence,” the process used, etc.), all to demonstrate that comparable data were actually used when approving the compensation.

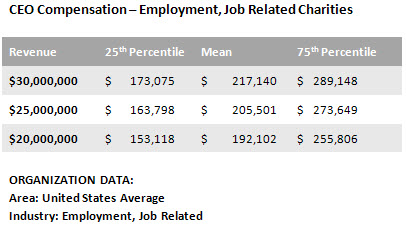

A first look at comparable data is easily obtained using ERI’s Nonprofit Comparables Assessor. With criteria that fit the search for a new CEO at Goodwill Industries Omaha (job title CEO, annual revenue size of $25 million, and nonprofit organization type of “Employment, Job Related”), the table below generated by the Nonprofit Comparables Assessor shows that the average annual compensation for this job in comparable organizations is expected to be around $206,000 per year. This is considerably less than the compensation paid to the CEO that just left the position.

When the geographic criteria in the Nonprofit Comparables Assessor was changed to Nebraska, there were too few observations to create a table, since there are not that many large (for Nebraska) employment organizations in the state. Recruitment for this position is likely to be national in scope, so the US average seems to be the most relevant for analyzing the market rate for this position.

The Omaha charity knows that regaining the trust and support of the public is an issue now and that many eyes will be focused on the compensation of the new CEO. Using comparable data to justify reasonable compensation levels as required by IRS rules and regulations is a significant first step in that process.