The discussion of whether or not the NFL should have nonprofit tax-exempt status is heating up again, as proposed federal legislation that would end such exemptions is considered (see http://ftw.usatoday.com/2014/09/nfl-tax-exempt for a discussion, which is more nuanced than it seems at first glance). Currently, the NCAA, NHL and PGA Tour do have similar non-profit status, while Major League Baseball gave up its non-profit status in 2007, and the NBA has never been tax-exempt. Of course, tax-exempt status does not mean that the NFL is considered a charity (serving the public good and accepting tax deductible contributions), just that it is a non-profit trade organization and doesn’t pay corporate income taxes. In fact, the NFL does pay taxes on some of its activities.

But, there are a lot of other nonprofit recreation and sports organizations in the nonprofit sector. The National Taxonomy of Exempt Entities, the classification system used in nonprofit research and in ERI’s Nonprofit Comparables Assessor, includes Major Group N – Recreation, Sports, Leisure, Athletics (shortened here as Recreation/Sports) as a part of the broader division of Human Services organizations. These organizations are included in this group:

- Recreational and Sporting Camps (Day, Overnight, etc.)

- Physical Fitness/Community Recreational Facilities (parks and playgrounds)

- Sports Training Facilities

- Recreational, Pleasure, or Social Clubs

- Fairs and festivals

- Amateur Sports Clubs, Leagues

- Olympics Committees and Related International Competitions

- Professional Athletic Leagues

This is a category that is wide ranging in size and influence, encompassing the village hunting club and social club as well as some state fairs, the NFL, and the Olympics Committee. Just computing an average of salaries for this group would be of very limited use to those wishing to set market-based salaries for their executives.

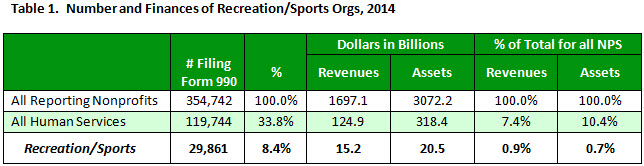

While close to one million nonprofit organizations are registered with the Internal Revenue Service in the United States (see IRS Exempt Organizations Master File, June 2014), only 37% of them have revenues that reach the level of $50,000 and meet the requirement to file a Form 990 each year (with the exception that all private foundations of any revenue or asset size must file a Form 990-PF). So, out of the almost 355,000 reporting tax-exempt organizations (meeting the revenue requirement for filing a Form 990), about 34% are involved in providing what is defined in the NTEE as Human Services. Although Human Services is by far the largest NTEE category of reporting nonprofits, Recreation/Sports organizations comprise only 8% of Human Services and less than 2% of all nonprofits. The table below shows how this group compares in annual revenues and assets to the rest of the nonprofit sector.

While Human Services organizations are over one-third of the total of reporting nonprofits, their revenues and assets represent a much smaller proportion of the total in the sector, at 7% and 10%, respectively. This finding is also evident with Recreation/Sports organizations at 8% of the total number of reporting nonprofits, but receiving only 0.9% of total sector revenue and holding only 0.7% of the total sector assets.

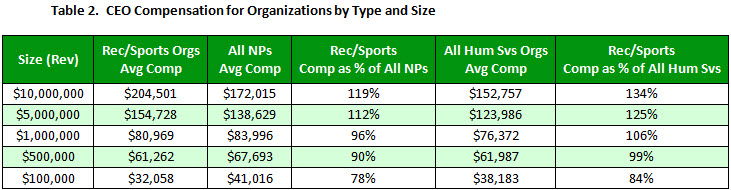

The disparities within the group are revealed by looking at the distribution of Recreation/Sports organizations by size, based on the annual revenues reported on their Forms 990. Of the nearly 30,000 organizations classified as Recreation/Sports, only about 9,000 of them reported paying any compensation at all. Of those, about 39% had revenues between $100,000 and $500,000, another 17% were in the $500,000 to $1 million range, and another 37% were in the $1 million to $10 million range. While the compensation of very large organizations are often in the press (for example, the NFL with a Commissioner salary of $44 million), the reality is that almost all of these organizations are very small. In fact, only around 60 have annual revenues of $50 million. Thus, when doing salary comparisons for CEOs, it is necessary to use data from similar-sized organizations not averages for the group.

ERI’s Nonprofit Comparables Assessor can be used to calculate average CEO salaries by size and type of nonprofit organization. The table below compares average CEO compensation for Recreation/Sports organizations with all nonprofits and then with all Human Services organizations. An interesting pattern emerges — at the lowest revenue ranges, salaries are lower than for both all nonprofit and Human Services averages, but that quickly changes as the organizations get larger. At the larger revenue sizes, Recreation/Sports organizations pay more than other nonprofits, especially those in Human Services. So the smallest ones pay less than other nonprofits, but those relationships change dramatically in larger organizations.

The IRS requires that public charities set executive salary levels looking at compensation data from similar organizations (typically defined as similar in type of service provided, size, and geographic location). Detailed comparisons using relevant data is clearly needed to ensure compensation levels that comply with IRS regulations. However, many of the organizations, particularly the larger ones, are classified as tax-exempt under the c6 subsection of the Internal Revenue Code – this means that they are not classified as charities (organized for the public good) and that compensation levels are not subject to IRS penalties. Their executive compensation must be reported annually on Form 990 and is public information; however, there probably won’t be an IRS investigation of salary levels. For smaller Recreation/Sports organizations, if they are tax-exempt as public charities (IRC Section 501c3), there is still a need to collect comparable data to set reasonable salaries, in accordance with IRS regulations.