It’s autumn, and thoughts of 2015 pay raises are forming in the minds of nonprofit leaders and their boards. At the least, this seems to be the season of the publications of annual reports about pay raises for nonprofit executives. Let’s review some of the findings of recent reports and see how helpful they will be for setting executive compensation that will be market-based and in line with IRS regulations.

Here are some key points from The Chronicle of Philanthropy’s annual compensation survey:

- Big nonprofits and foundations are beginning to finally pay executives more than the inflation rate, with a median increase of 4.9% between 2011 and 2012 (The Chronicle tracks only 82 organizations, the largest charities in the US.).

- Excluding the 20 groups that cut pay or kept it flat, the remaining 62 organizations in The Chronicle’s survey increased CEO pay 6.8% in 2012.

- Compensation was more than $2 million for 18 CEOs.

GuideStar’s annual study was also released this week and gives a broader view of increases in the sector, as the research includes data from about 91,000 organizations. Consider these findings:

- The median pay increase for top executives at nonprofits was 2.2% in 2012, up from 2% in 2011 and 1.6% in 2010.

- There is a significant gap between pay in larger and smaller charities, and it appears to be widening. For CEOs in the largest charities, the median increase was about 4% in 2012 (median salary of $444,108), while the average increase for heads of charities with less than $250,000 was approximately 1% (median salary of $44,806).

So what is the “right” increase for 2015? Using these reports, one could conclude a range between 1% and 7% – of course, the reports are of CEO pay increases between 2011 and 2012. Obviously, those determining an annual pay raise for a charity executive must do research far beyond reading some averages and medians for the nonprofit sector as a whole or even the groupings available in these reports.

The factors that influence compensation remain the same: what you do (the job) and where you do it (type, size, and sometimes location of organization). The data that are needed for comparison must be collected from similar organizations, and what is important to the market is the salary paid, not the rate of increase. The rate of increase for a CEO in a specific organization should be based on how the current pay aligns with the market rate for the position as determined by the comparable data. Overall averages and medians always seem to be of great interest but often are a poor basis to determine market rates that follow IRS criteria.

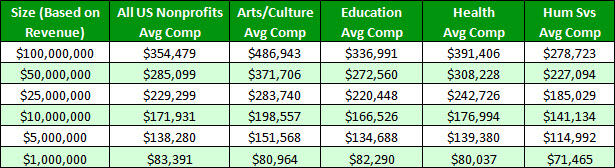

For example, the table below, created using ERI’s Nonprofit Comparables Assessor, illustrates the variation in pay for different sizes and types of nonprofit organizations. It also shows the danger in applying an average or median increase to a salary to attempt to come up with CEO compensation.

Table 1. Average Nonprofit CEO Compensation by Type and Size

The differences in average CEO pay among large and small organizations are huge, but the differences among organizations with varying activities and services are also striking. Obviously, just applying an average or median increase from a survey such as those cited above may not bring about a compensation level based on what is paid by comparable organizations.

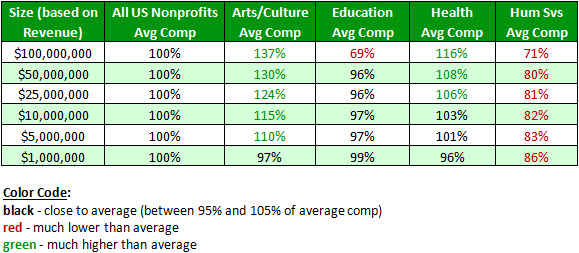

To further illustrate, Table 2 shows how average CEO compensation for different types of organizations varies from the all nonprofit average at different sizes. Again, it is clear that both the factors of type of organization and size influence compensation levels.

Table 2. CEO Compensation for All Nonprofits Compared to Different Types and Sizes

The only way to assess appropriate compensation levels is to look at levels for comparable organizations, using type of organization and the size as major factors. In some types and sizes, geographic location will also be a factor. Although this is a much more detailed analysis than reviewing more general national surveys, it is easily accomplished using ERI’s Nonprofit Comparables Assessor. Nonprofit boards will then be assured that their CEO compensation is competitive and their process is in compliance with IRS standards.