In New York State, when the state legislature failed to act to place caps on executive salaries in nonprofits providing state-funded human services, the state implemented regulations to achieve the same goal (see http://executiveorder38.ny.gov/ for more information). However, State Supreme Court Judge Thomas Feinman of Nassau County rejected those caps in a recent decision on a lawsuit by the Agencies for Children’s Therapy, a non-profit that represents more than 30 agencies that provide early intervention, prekindergarten, special education and other services to children throughout the state. More information is available here.

The judge thought that the Department of Health had overstepped its boundaries and noted that the state legislature had already rejected similar proposals.

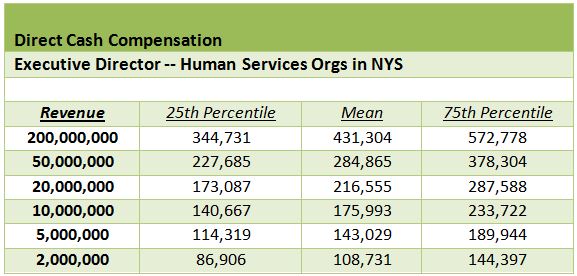

No information is available on whether or not the state will appeal this ruling, but an analysis of the Form 990 data on salaries for New York State (NYS) nonprofits that provide human services and typically receive state funds show why the salary caps were of concern to the nonprofits. As is typical, the mean salaries for executive directors increased with the size (based on annual revenues) of the organization. ERI’s analysis using the Nonprofit Comparables Assessor shows that an organization with revenues of $20 million or more on the average pays its executive director more than the cap of $199,000.

Some of the NYS human services organizations included in the above calculation may not be covered under the current salary cap regulations as they may not receive state funds to provide services, or may be exempt from the cap for some other reason. But the table above does provide information on the market rate for executive directors of these types of organizations. For those covered by the cap, there would be a significant impact.

The IRS regulations call for salary data for similar nonprofits to be used in salary determination, and typical criteria to determine comparability include size, location, and type of services provided. The IRS does not use arbitrary salary caps but requires that the executive boards setting the salaries look at appropriate comparable data.

The salary data do indicate why NYS human services organizations are concerned about the salary cap and why a lawsuit was launched. The table below details the number of NYS organizations in each of three different size categories (roughly small, medium and large), with an estimate of the number and percent of organizations impacted by the salary cap.

It is clear that an arbitrary salary cap does not take into account one of the main criteria for setting salaries — size of the organization. It appears that larger organizations in NYS will especially have a difficult time attracting and retaining top executives if the salary cap is fully implemented.